New Regulations on Alternative Lending: What Every Borrower Needs to Know!

2025-01-22

Author: William

Introduction

The landscape of alternative lending in Canada has drastically shifted with new regulations that took effect on January 1, 2024, aimed at curbing predatory lending practices. These reforms target high-interest and payday loan sectors, which have drawn scrutiny for exploiting vulnerable populations, especially in low-income communities.

Background of the Regulations

Initially proposed by the federal government in 2023, these changes update the 'Criminal Interest Rate Regulations,' addressing serious concerns over the practices of predatory lenders. Two major reforms stand out: a cap on payday loan fees and a restriction on the interest rates applicable to various loans.

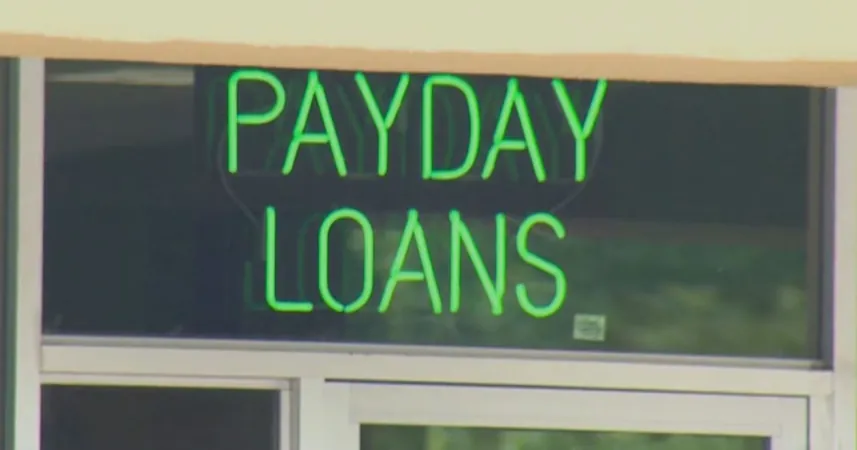

Payday Loan Fee Cap

Doug Hoyes, a licensed insolvency trustee at Hoyes, Michalos and Associates, has emphasized that the new cap on payday loan fees is set at $14 per $100 borrowed. While this regulation is designed to assist consumers, Hoyes points out that payday loans remain one of the costliest borrowing options available. "If you’re paying $14 and have to repay it within two weeks, that equates to an eye-watering 364% interest over a year," he stated.

Interest Rate Restrictions

Further developments now restrict high-interest loans as well. Previously, lenders could charge an alarming interest rate of up to 47.9%—a number that has now decreased to a maximum of 35%. This change is particularly critical for those with poor credit, as the ceiling on interest rates offers some relief but may simultaneously shut out many potential borrowers. Peter Kalen, CEO of Money Mart, expressed concern that while some clients may benefit, many in dire need of financial assistance may find themselves unable to secure loans. "As a result, we're seeing people turned away and pushed towards illegal lending options," Kalen remarked.

Industry Response

The industry response suggests that the tightening of regulations may inadvertently displace borrowers to riskier, unregulated alternatives. Bruce Sellery, CEO of Credit Canada Debt Solutions, noted, "Consumers who can't qualify for traditional loans might resort to payday lenders or even the black market for cash." Both experts and advocates are calling on the federal government to take further action against illegal lenders, establishing a safer borrowing environment for all Canadians.

Advocates' Perspective

On a brighter note, numerous advocates are heralding these changes as a significant step towards alleviating the debt cycle for many borrowers. These new regulations can pave the way for individuals to improve their credit scores over time, opening doors to loans with lesser interest rates and ultimately saving money.

Importance of Good Credit Ratings

As a precautionary measure, these developments stress the importance of timely bill payments. Maintaining a good credit rating becomes essential, as a lower score can severely limit access to essential financial products like car loans, mortgages, and credit cards.

Conclusion

In conclusion, while the new regulations bring positive changes, borrowers should remain vigilant and informed. Understanding these laws can empower consumers to make better financial decisions in an evolving lending landscape.

Brasil (PT)

Brasil (PT)

Canada (EN)

Canada (EN)

Chile (ES)

Chile (ES)

Česko (CS)

Česko (CS)

대한민국 (KO)

대한민국 (KO)

España (ES)

España (ES)

France (FR)

France (FR)

Hong Kong (EN)

Hong Kong (EN)

Italia (IT)

Italia (IT)

日本 (JA)

日本 (JA)

Magyarország (HU)

Magyarország (HU)

Norge (NO)

Norge (NO)

Polska (PL)

Polska (PL)

Schweiz (DE)

Schweiz (DE)

Singapore (EN)

Singapore (EN)

Sverige (SV)

Sverige (SV)

Suomi (FI)

Suomi (FI)

Türkiye (TR)

Türkiye (TR)